Former Green Valley Ranch HOA Manager 'Shocked' At HOA's Cash Stash

DENVER (CBS4)- Roger Sherman, who managed the Green Valley Ranch HOA for 15 years, says he was "shocked" to learn the current HOA board has amassed more than $1 million in cash, savings accounts, checking accounts and CDs while simultaneously initiating foreclosure proceedings against homeowners who haven't paid their HOA penalties.

"It just seems unfair," said Sherman.

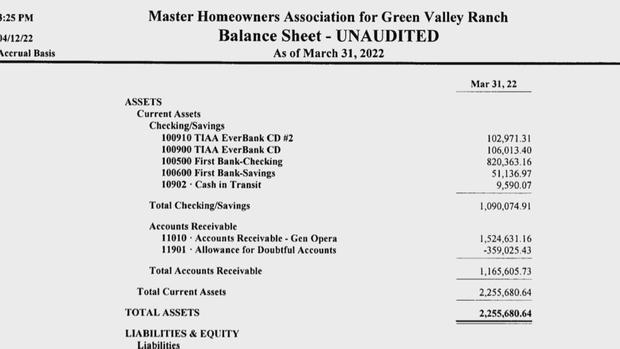

A CBS4 Investigation this week reported that the controversial HOA had accrued $1,090,074 in cash and equivalent assets, an amount that has been building up in its bank accounts for the last four years according to the HOA's own financial reports. In 2021, the HOA initiated more foreclosures against its residents than any other Denver HOA. An examination of the HOA's financial records shows it typically collects between $300,000 to $600,000 in covenant fines each year.

"I was just shocked," said Sherman. "Times have changed since I was out there."

Sherman told CBS4 he was the property manager for the HOA from 1991 until 2004 but that the HOA hardly ever initiated foreclosure proceedings.

"Associations are about being good neighbors, not pushing people out," he said.

He said he was confused about why the current HOA board is collecting so much in fees.

"If you have $1 million in the bank, it just makes no sense," said Sherman.

Current HOA board members did not respond to multiple emails from CBS4. On a visit to the home of board member and treasurer Alvina Ferguson, she said, "That's all fake... it is all fake."

She declined to offer further comment.

The HOA, which oversees 4,600 homes, released an earlier statement that its foreclosure filings amount to less than 1%, which they contend is similar or below other HOAs in Colorado.

Stan Hrincevich with the Colorado HOA Forum, a homeowners advocacy organization, said after reviewing the GVR HOA's financial statements, "Something just doesn't seem right. Where are we going with this? It's out of control."

Hrincevich suggested with more than a million dollars in the bank, the HOA could be using that surplus to reduce assessments on homeowners, return money directly to residents or take on more maintenance responsibilities for homeowners who have fallen behind.

"I really hope those folks find some reform out there," said Hrincevich.